If you have health insurance coverage, the most that you’ll have to pay for covered medical services in a year is called your out of pocket maximum. Depending upon the plan you have, “covered services” can differ and your out of pocket maximum will vary from that of other plans. To learn more about rehab insurance costs, call us to verify your insurance today.

What costs go towards meeting the out of pocket maximum?

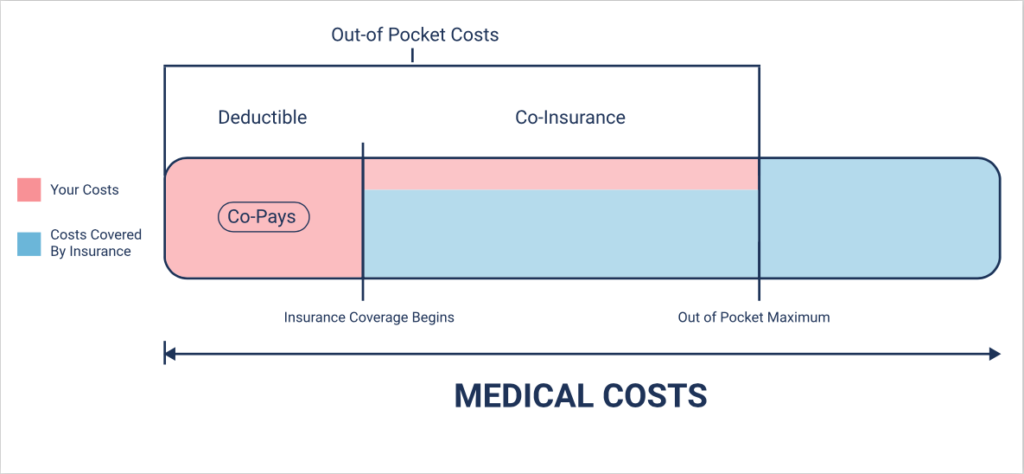

It’s important to know what costs you pay out of pocket. Listed below are some costs included in most medical insurance plans:

Deductible

Your deductible is the set amount of cash you have to spend on medical costs prior to insurance kicking in and starts supporting your medical expenses. Typically, any expenses that go towards meeting your deductible likewise go towards your out of pocket maximum.

Coinsurance

This amount comes as a percentage. With most plans, after you’ve satisfied your deductible you and your insurance split the cost of your competent medical costs. If your coinsurance is 20%, then after the deductible is met, you will pay 20% of medical bills and your insurer will pay the remaining 80%.

Copayment

Unlike coinsurance, this is a fixed rate you pay for healthcare at the time that you require it. When you visit the medical professional or health center, your policy may have an outlined quantity such as $40 for office visits and $250 for a hospital visit that you will need to pay.

Premiums

The regular monthly premium does not go towards your maximum out of pocket expenses. Even after you have actually met your out of pocket maximum, you will continue paying your monthly premium unless you cancel the policy, or change to a new policy during the open enrollment period.

Medical services that you pay for, and that not covered by your policy, will not count towards your out of pocket maximum.

Do I have a copayment after meeting the out of pocket maximum?

This is a common question that arises, but it’s simple to answer if you understand the technical definitions for both of these health insurance terms. A copayment is an out of pocket payment that you make towards typical medical expenses like doctor’s office visits or an emergency room visit. An out of pocket maximum is the set amount of money you will have to pay in a year on covered medical expenses. In many plans, there is no copayment for covered medical services after you have met your out of pocket maximum. All policies are different though, so make sure to take notice of plan details when buying a policy. If you’ve already purchased a policy, you can take a look at your copayment details and make certain that you’ll have no copayment to pay after you’ve met your out of pocket maximum.

Though, after you’ve satisfied the set limitation for out of pocket expenses, insurance coverage will be paying for 100% of covered medical expenses.

Does my out of pocket maximum include my deductible?

Yes. That is the short answer, but understanding the definitions of out-of-pocket maximums and deductibles will help you know what is included. The deductible is the amount you will need to pay out of pocket before the insurer will help cover the costs of your medical bills. Your out of pocket maximum is the maximum amount you will need to pay whatsoever.

So, if you go to the emergency room and are charged $1,000, you will have to pay this first but it will get you closer to fulfilling both the deductible and out of pocket maximum.

Low out of pocket maximum.

Based on the definition of how out of pocket maximums work, it might seem like you should always go for the policy with the least out of pocket max. However, that’s not the case for everybody.

For some people it will help to have a low deductible and out of pocket maximum. They will immediately fulfill those levels and have insurance cover almost all of their medical costs. If you’re somebody who does not anticipate to spend thousands of dollars on medical costs early on in the year, you may not satisfy your out of pocket maximum regardless of whether it’s high or low. Frequently plans with low deductibles and out of pocket costs come with higher premiums. So if you do not anticipate to meet your out of pocket maximum before the end of the year, it might be more economical for you to choose a policy with a lower premium.

Each policy has its own terms and limitations, so make sure to check the official plan documents to comprehend how that particular plan works. This post is just for general education.